Written By: Andy Posner, Capital Good Fund & Attorney Kelly Ryan, Ryan Immigration Group

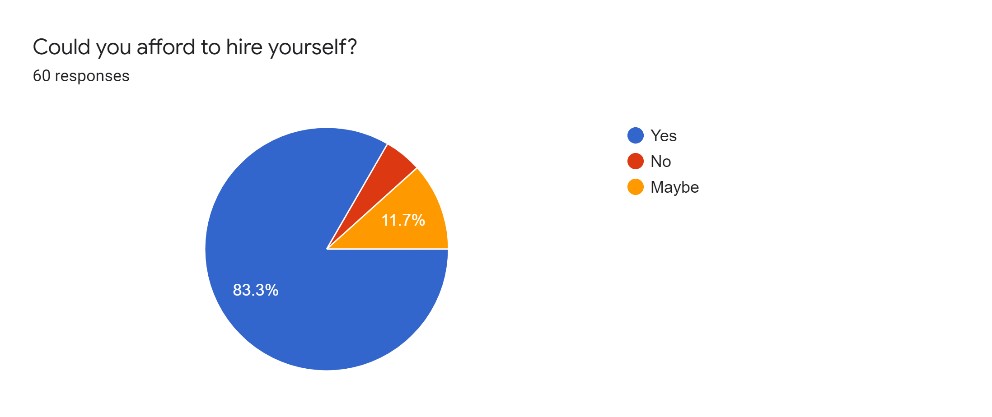

How many times have you squirmed in your seat after quoting a reasonable fee, for a more than deserving client, and getting this sincerely shocked response? Our firm is fee transparent: we publish them on our website and tell people before they book a consultation, yet some are still taken aback. And look, I get it. Most people in our country cannot come up with $400 to cover an emergency; in a recent survey of the members of our Colorado AILA Chapter, 16.7% of attorney respondents were unsure if they could afford to hire themselves.

“We Don’t Talk About The Benjamin’s No, No, No!”

Yet avoiding the fee discussion is ineffective. Money could be an inherent conflict of interest, a zero-sum battle between clients and attorneys. However, it doesn’t have to be if done right, the fee is a win-win, a natural and expected part of the client experience.

To get to the win-win fee discussion, first start by educating clients on what you will do and the value that will bring to their lives. Then, welcome your potential clients to your firm. Set them up for success by explaining confidentiality, privilege, and the team members they will work with. Don’t get bogged down in the details, but let them know that they’ll have plenty of support during the case.

Third, build trust with your clients. Go through the intake with them. Get them comfortable talking to you; find a sincere way to connect. As clients answer more of the easy questions, it will be easier to answer the harder questions and find the best strategy for their issue.

Fourth, figure out potential solutions, including approximate timelines for milestones. Qualify that processing times are a disaster now; pre-Trump and pre-pandemic expectations are out the window, but the government has proposed goals that they hope to reach by 2024. Discuss fees when you discuss the options, don’t leave it until the very end! They’ll get lost in the numbers without the immediate context of the work you propose.

Provide Financing Options

Doing an amazing consultation is a waste of time for everyone unless you are hired to work the case.

Remember that the case is an investment on the part of your client: they are investing in their future, dreams, and families. The data is clear: undocumented workers earn 35% of documented workers; mortgage and auto loan rates for those with an ITIN are much lower than for those with an EAD or temporary status. As with any investment, coming up with the funds is a crucial question.

Payment plans are an obvious option, but firms shouldn’t overextend themselves on these. Make sure that the client will have paid you what it is owed at each benchmark. And always require autopayments with an ACH with any payment plan, lest you find yourself perpetually waiting for the “check in the mail” to arrive, wasting time with unpleasant “collection” work, or paying 2-3% merchant fees plus swipe fees. The downsides of payment plans include the fact that you are now the client’s attorney and lender and that you will inevitably not collect 100% of what you are owed, impacting your revenue, community goodwill, and conscience.

Another option is to offer a loan product. We refer to Capital Good Fund, a nonprofit lender that is AILA’s National Preferred Loan Partner. They offer low rates, long terms, report payments to the credit bureaus—and, crucially, get you out of the business of servicing payment plans so that you can focus on the case. They operate in ten states (RI, MA, FL, DE, TX, MA, NJ, CT, CO, GA), with more expansion planned—you can learn more here. If they are not in a state where you operate, carefully consider where you refer clients. Credit unions and local banks tend to be the most trustworthy, although they can have more restrictive credit guidelines. Lastly, be sure that your client knows that your relationship with the lender is separate and that you cannot guarantee the outcome of their application.

Depending on your client’s needs and the jurisdiction, check out credit unions and other nonprofits for low-interest rates. In Colorado, Fitzsimmons Credit Union has a $1000 no-interest DACA loan; in California Mission Asset Fund has 0% filing fee loans. Credit unions and non-profits have prohibitively low caps or are specifically for filing fees, unlike Capital Good Fund.

Some attorneys refer to for-profit private lenders who also market their services as payment plan administrators. PROCEED WITH CAUTION! Interest rates are often above 30%, and have low loan approval rates with aggressive collection processes. Do not ruin your relationship with clients by associating with a predatory lender.

At The End Of The Day..

The reality is that you have to charge a fee that enables you to thrive as a firm. Customers will usually understand that, if you are transparent about your fees, and if you give them options for paying. A frank conversation about payment options will open the door to more families—those most in need of your services—to be able to access high-quality legal advice and realize the benefits of an improved legal status.